Financial experts have long extolled the guarantee of reverse home loans https://heldazns37.doodlekit.com/blog/entry/16646779/the-buzz-on-how-does-the-trump-tax-plan-affect-housing-mortgages to increase earnings for retirement-age households. Lots of older house owners own significant equity in their houses. The real estate wealth of house owners 62 and older struck a record $7. 7 trillion in the second quarter of this year, according to the National Reverse Home Loan Lenders Association.

So, reverse home loans (for those who own houses) can be extremely appealing. Only 33,000 reverse home loans were originated in 2018, however, according to The Urban Institute think tank. That's a mere 1. 3% of the 2. 5 million loans homeowners secured to draw out equity through credit lines, cash-out refinancing and home equity loans.

19 million households have actually taken out the federal government's Federal Real estate Administration-insured reverse mortgages to assist them meet their monetary needs. "We live in a world where (reverse home loans work) for a little group of individuals," says Individual retirement account Rheingold, executive director of the National Association of Consumer Advocates in Washington D.C.

How Do Balloon Fixed Rate Mortgages Work? Things To Know Before You Buy

The dangers are specifically uneasy for lower-income property owners whose financial resources are so fragile, they risk of missing payments of residential or commercial property taxes and homeowner's insurance. Necessary therapy sessions prior to taking out a reverse home mortgage assistance, however the sessions are brief. Thomas Davidoff, professor of property financing at the UBC Sauder School of Organization in Vancouver, recalled a conversation he had on a flight with a seatmate from Florida who had actually secured a reverse mortgage.

Thomas Davidoff When Davidoff asked her why, she said that "she was the only one who might figure it out and the just one without kids," he says. Not having the ability to hand down the house to successors gives misunderstanding amongst lower-income, reverse-mortgage debtors. Many individuals in low-income neighborhoods reside in multigenerational houses.

" What we hate to see is property owners participate in a reverse home loan without understanding it won't pass it on to beneficiaries. who issues ptd's and ptf's mortgages. The beneficiaries can rarely afford to re-finance or settle that worth," states Savage. Adds Odette Williamson, staff attorney at the National Consumer Law Center in Boston: "So when grandmother loses the home, the daughter and others likewise lose the home." While reverse mortgages can be a valuable source of retirement earnings for some, the dangers can be serious for older, low-income borrowers.

The 7-Second Trick For How Many Mortgages In One Fannie Mae

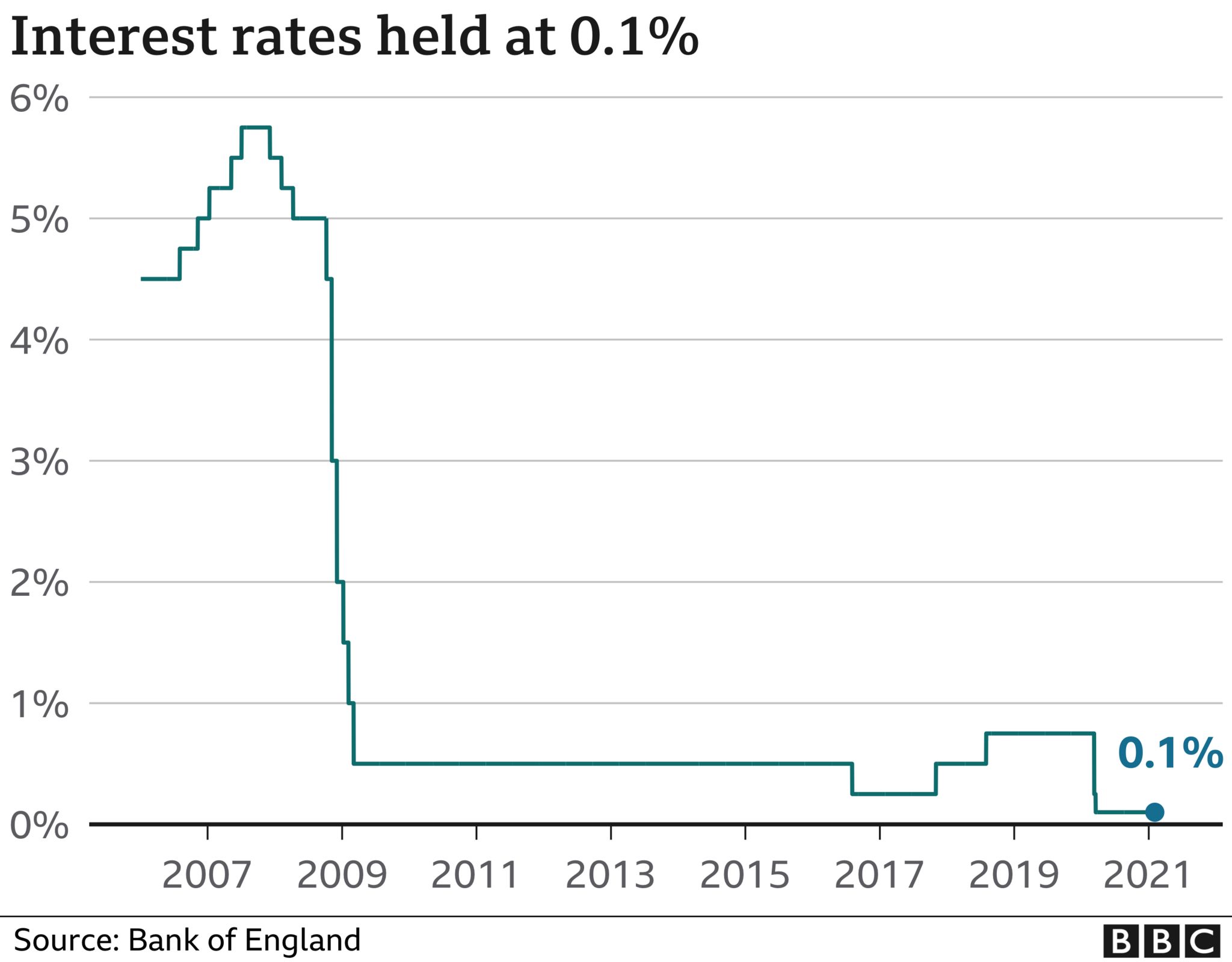

That's since of the federal government's pandemic-induced foreclosure moratorium that lasts through year-end. Once the moratorium lifts, experts state, reverse home loans will practically definitely shoot up. Other reverse mortgage reforms recently have made the loans much safer than in the past, nevertheless. For instance, to receive a reverse home mortgage, there's now a cost test to see if you are likely to be able to continue making the required payments.

Democratic Representatives Maxine Waters of California and Denny Heck of Washington have actually sponsored legislation to help avoid timeshare trade reverse-mortgage home losses by needing loan providers to do more to avoid foreclosure. "A reverse home mortgage isn't naturally bad, and they're more secure than they utilized to be," says Hulstein. However the reverse mortgage still has a long method to precede it ends up being a standard option for the common retirement-age homeowner.

Chris Farrell is senior economics contributor for American Public Media's Marketplace. Discover more unheard stories about Kansas City, every Thursday. Check your inbox, you must see something from us. Power Kansas City reporters to inform stories you enjoy, about the community you love. Donate to Flatland.

The Of Bonds Payment Orders, Mortgages And Other Debt Instruments Which Market Its

If you're 62 or older and want cash to settle your home loan, supplement your earnings, or spend for healthcare expenditures you might think about a reverse mortgage - what is the going rate on 20 year mortgages in kentucky. It enables you to transform part of the equity in your house into money without needing to sell your house or pay extra regular monthly expenses.

A reverse home loan can use up the equity in your house, which suggests fewer assets for you and your heirs. If you do decide to look for one, examine the different types of reverse mortgages, and contrast store before you choose a particular company. Keep reading to read more about how reverse mortgages work, receiving a reverse home mortgage, getting the best offer for you, and how to report any fraud you might see.

In a mortgage, you get a loan in which the lending institution pays you. Reverse mortgages take part of the equity in your home and transform it into payments to you a sort of advance payment on your home equity. The cash you get typically is tax-free. Typically, you do not have to repay the cash for as long as you live in your home.

The Ultimate Guide To What States Do I Need To Be Licensed In To Sell Mortgages

In some cases that implies offering the house to get cash to repay the loan. There are 3 type of reverse home loans: single function reverse home mortgages used by some state and local government firms, in addition to non-profits; exclusive reverse mortgages private loans; and federally-insured reverse mortgages, also referred to as House Equity Conversion Mortgages (HECMs).

You keep the title to your home. Instead of paying month-to-month mortgage payments, though, you get a bear down part of your home equity. The cash you get generally is not taxable, and it generally will not affect your Social Security or Medicare benefits. When the last enduring borrower passes away, offers the house, or no longer lives in the house as a principal home, the loan needs to be paid back.

Here are some things to consider about reverse home loans:. Reverse home loan lenders generally charge an origination fee and other closing expenses, as well as servicing charges over the life of the home mortgage. Some likewise charge home loan insurance premiums (for federally-insured HECMs). As you get cash through your reverse home mortgage, interest is included onto the balance you owe monthly.

What Are Cpm Payments With Regards To Fixed Mortgages Rates Fundamentals Explained

A lot of reverse mortgages have variable rates, which are tied to a monetary index and change with the market. Variable rate loans tend to provide you more choices on how you get your cash through the reverse home mortgage. Some reverse mortgages mainly HECMs use fixed rates, but they tend to require you to take your loan as a lump sum at closing.

Interest on reverse home loans is not deductible on tax return until the loan is paid off, either partially or completely. what lenders give mortgages after bankruptcy. In a reverse home mortgage, you keep the title to your house. That suggests you are accountable for property taxes, insurance coverage, energies, fuel, maintenance, and other costs. And, if you do not pay your real estate tax, keep house owner's insurance, or maintain your house, the lending institution may need you to repay your loan.

As a result, your lending institution might need a "set-aside" total up Additional info to pay your taxes and insurance coverage throughout the loan. The "set-aside" lowers the amount of funds you can get in payments. You are still accountable for maintaining your home. With HECM loans, if you signed the loan documentation and your partner didn't, in particular scenarios, your partner might continue to reside in the house even after you die if she or he pays taxes and insurance, and continues to preserve the property.