The goal is that, through this conference, you will have the ability to make an informed decision about whether a reverse mortgage is best for your circumstance. Currently, about 40% of older adults who meet a HECM counselor choose to go forward with the process. If you have an interest in taking out a reverse home loan, one location you may wish to use through is a member of the National Reverse Home Mortgage Lenders Association to help prevent rip-offs.

As far as expenses associated with getting a reverse home mortgage, a number of them could be paid out of the loan profits, implying that you would not have to pay them expense. Nevertheless, financing loan costs minimizes how much cash will be readily available for your needs. Fees involved consist of but might not be restricted to: Upfront fee: 2% of the house's evaluated worth iof FHA providing limitation (whichever is less) Yearly cost: 0.5% of the exceptional loan balance Your loan provider can let you know which of these are obligatory for you.

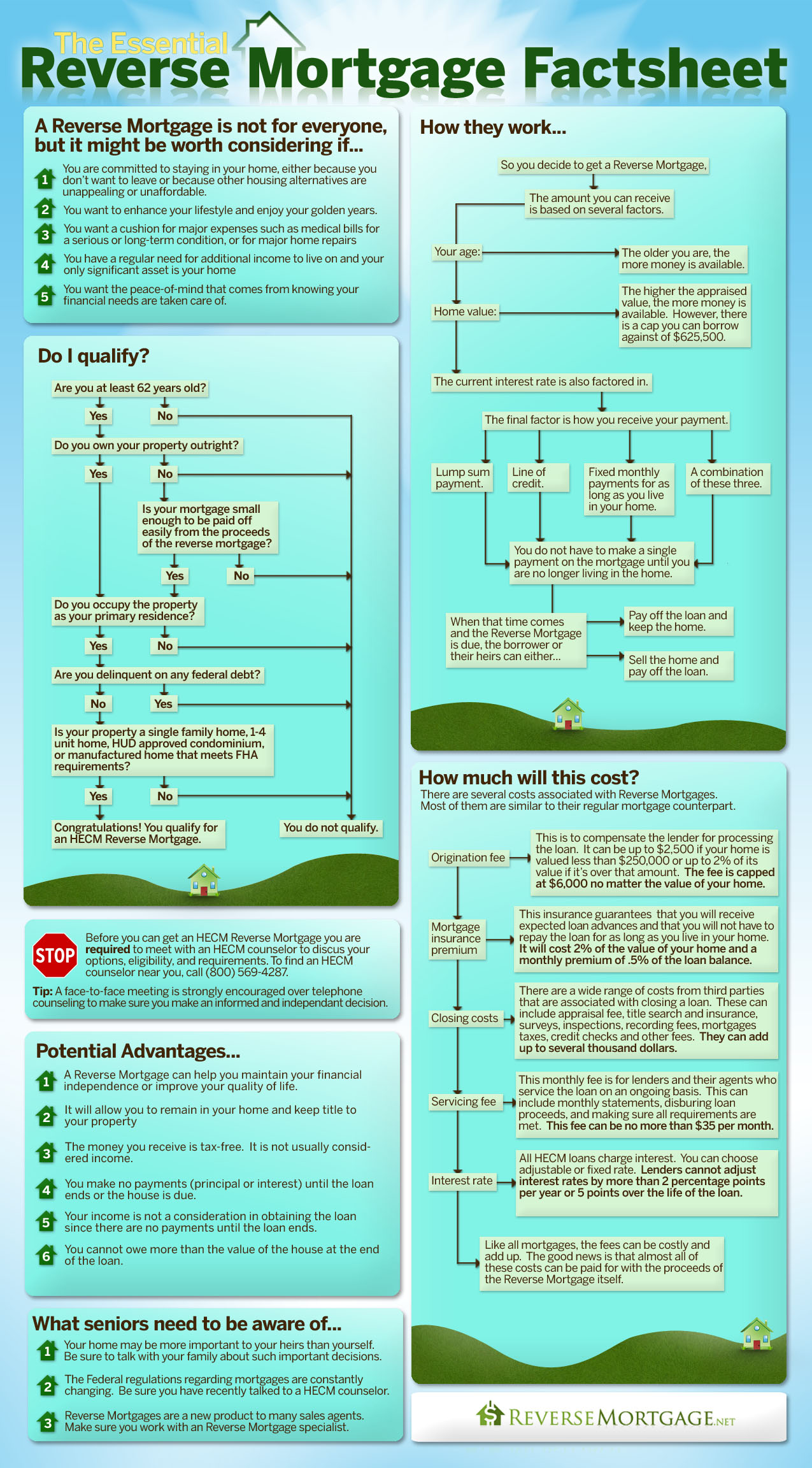

A lender might charge an origination cost as follows: the greater of $2,500 or 2% of the first $200,000 of the home worth, plus 1% of the amount over $200,000 (what are the current interest rates for mortgages). The origination cost cap is $6,000. A loan provider or agent services the loan and verifies that property tax and risk insurance premiums are kept existing, sends you account declarations, and pays out loan profits to you.

The 4-Minute Rule for Who Does Usaa Sell Their Mortgages To

The regular monthly service charge can not go beyond $30 if the loan interest is fixed or changes every year. If the interest rate can adjust monthly, the maximum regular monthly service fee is $35. Third-party costs that might exist when obtaining the loan include an appraisal, surveys, examinations, title search, title insurance coverage, recording fees, credit checks, etc.

For one, unlike many loans, you do not need to make any monthly payments. The loan can be utilized for anything, whether that's debt, healthcare, daily costs, or buying a villa. How you get the cash is also flexible: You can select whether to get a swelling amount, regular monthly disbursement, credit line, or some mix of the three.

If the house is cost less than the amount owed on the mortgage, Customers may not need to pay back more than 95% of the house's assessed worth since the home loan insurance coverage paid on the loan covers the rest. You can also utilize a reverse home mortgage to purchase a main house if you have sufficient funds for the down payment (you essentially require to pay about half of the home's price utilizing your own cash and savings), along with the ability to spend for other home costs, such as real estate tax and insurance (which type of interest is calculated on home mortgages?).

What Does How Do Reverse Mortgages Work Example Mean?

If you move out of your home, the loan can also end up being due. Reverse home mortgage interest rates can be fairly high compared to https://www.liveinternet.ru/users/adeneu3zfl/post474541318/ traditional home loans. The included expense of mortgage insurance coverage does use, and like many mortgage, there are origination and third-party costs you will be accountable for paying as explained above.

If you decide to take out a reverse home loan, you may desire to speak to a tax consultant. In basic, these earnings are not thought about gross income, however it might make good sense to learn what holds true for your particular circumstance. A reverse home loan will not have an effect on any routine social security or medicare benefits.

Depending on your financial needs and goals, a reverse mortgage might not be the best alternative for you. There are other ways to use money that might offer lower fees and don't have the very same stiff requirements in terms of age, home value, and share of home loan paid back such as a home equity line of credit or other loan alternatives.

Some Ideas on How Do Interest Rates Affect Mortgages You Need To Know

An individual loan may be a great alternative if you need to settle high-interest debt, fund house renovations, or make a big-ticket purchase. A personal loan may be an excellent option if you require to settle high-interest debt, fund house renovations, or make a big-ticket purchase. SoFi uses personal loans ranging from $5,000 to $100,000, and unlike with a reverse home mortgage, there are no origination costs or other covert costs.

SoFi makes it simple to make an application for an unsecured individual loan with a simple online application and live client support 7 days a week. Another alternative is a cash-out refinance, which involves securing a loan with new terms to re-finance your home loan for more than you owe and taking the distinction in money.

Cash-out refinances may be a good option if the new loan terms are beneficial and you have enough equity in your house. If you do not have or don't wish to pull extra equity out of your house, you might think about an unsecured individual loan from SoFi. The details and analysis provided through links to 3rd party websites, while thought to be precise, can not be guaranteed by SoFi.

The Greatest Guide To How Are Adjustable Rate Mortgages Calculated

This short article supplies basic background details just and is not intended to act as legal or tax recommendations or as a replacement for legal counsel. You ought to consult your own lawyer and/or tax advisor if you have a concern requiring legal or tax advice. SoFi loans are come from by SoFi Lending Corp (dba SoFi), a lender certified by the Department of Company Oversight under the California Funding Law, license # 6054612; NMLS # 1121636 .

The following is an adjustment from "You Do not Need To Drive an Uber in Retirement": I'm normally not a fan of monetary products pitched by previous TV stars like Henry Winkler and Alan Thicke and it's not because I as soon as had a shouting argument with Thicke (real story). When financial products need the Fonz or the daddy from Growing Discomforts to convince you it's a great concept it most likely isn't.

A reverse home mortgage is sort of the reverse of that. You already own your home, the bank offers you the money in advance, interest accumulates each month, and the loan isn't repaid till you pass away or move out. If you die, you never repay the loan. Your estate does.

Excitement About What Percentage Of Mortgages Are Fannie Mae And Freddie Mac

When you get a reverse home loan, you can take the cash as a lump sum or as a credit line anytime you desire. Sounds good, best? The truth is reverse home mortgages are exorbitantly costly loans. Like a regular mortgage, you'll pay various charges and closing costs that will total thousands of dollars.

With a routine home mortgage, you can prevent spending for mortgage insurance coverage if your deposit is 20% or more of the purchase rate. Because you're not making a down payment on a reverse home loan, you pay the premium on mortgage insurance coverage. The premium equals 0.5% if you get a loan equal to 60% or less of the assessed value of the home.

If your house is appraised at $450,000 and you secure a $300,000 reverse home loan, it will cost you an additional $7,500 on top of all of the other closing expenses. You'll also get charged roughly $30 to $35 per month as a service charge. The overall is charged based upon your life span (what is the interest rate on reverse mortgages).