The types of forbearance readily available differ by loan type. If you can't make your home loan payments since of the coronavirus, start by comprehending your alternatives and connecting for assistance. As you prepare for the possible spread of the coronavirus or COVID-19, here are resources to safeguard yourself financially. Federally-held trainee loan payments are postponed and interest has been waived.

An adjustable rate home loan is one in which for the very first numerous years of the loan, the rate is repaired at a low rate. At the end of the set period, the rate adjusts once per year up or down based on an index contributed to a continuous margin number. In the preapproval procedure, your prospective loan provider does all the deep digging and exploring your financial background, like your credit report, to verify the kind of loan you could get, plus the interest rate you 'd receive. By the end of the process, you need to know exactly just how much money the loan provider wants to let you obtain, plus a concept of what your home mortgage schedule will appear like.

Mortgage applicants with a rating greater than 700 are best poised for approval, though having a lower credit report won't immediately disqualify you from getting a loan. Cleaning up your credit will eliminate any doubt that you'll be approved for the best loan at the ideal rates. Once you have actually been approved for a mortgage, handed the secrets to your brand-new house, moved in and started repaying your loan, there are some other things to remember (what are the interest rates on reverse mortgages).

Facts About How Do Mortgages Work In The Us Uncovered

Your PMI is likewise a sort of security; the additional money your pay in insurance (on top of your principal and interest) is to make certain your loan provider makes money if you ever default on your loan. what are the different types of home mortgages. To avoid paying PMI or being perceived as a risky customer, only buy a house you can manage, and objective to have at least 20 percent down prior to obtaining the rest.

Initially, you'll be responsible for commissions and additional charges paid towards your broker or property representative. Then there'll be closing expenses, paid when the home loan process "closes" and loan payment starts. Closing costs can get pricey, for lack of a better word, so brace yourself; they can range in between 2 to 5 percent of a home's purchase rate.

Home loans exist in a completely different measurement than the typical apartment or condo lease, so if you're seeking to make the transition from leasing to purchasing, be familiar with your house providing basics, and more, to to eliminate all doubt and proceed with self-confidence as part of the homeowners club.

What Is An Underwriter In Mortgages - An Overview

So, you're thinking of purchasing a home. This suggests you probably require to get a. Considering that you'll be paying your mortgage for many years to come, it's necessary you discover the right loan with the most beneficial terms possible. While this indicates you need to go shopping around among different loan providers, it's likewise important to get your monetary Continue reading life in order so you're an appealing borrower who's all set to pay your home mortgage bills - what are reverse mortgages and how do they work.

When you purchase a house, you can't fund the entire cost. You require a deposit. In truth, purchasers are expected to put 20% down on a house-- so if you buy a $300,000 home, you should have a down payment equivalent to $60,000. Most house purchasers do not have a 20% down payment.

And, for some loans guaranteed by the federal government-- such as FHA loans-- you can qualify for a home loan with a down payment as low as 3. 5%. This is among the top lending institutions we've used personally to secure big cost savings. No commissions, no origination fee, low rates.

The Of What Is The Harp Program For Mortgages

Conserving up a 20% deposit enables you to prevent paying home mortgage insurance, which costs around. 5% to 1% of the borrowed amount on a yearly basis. Home loan insurance safeguards the bank if you default, but you pay for it. Possibly more importantly, having a considerable down payment implies you're unlikely to end up owing more than your house is worth.

In reality, by the time you think about the expenses of selling-- consisting of 6% commission to a real estate agent plus other closing costs and move taxes-- home costs would barely have to fall at all before you wind up in a scenario where you need to bring cash to closing even if you put 10% down.

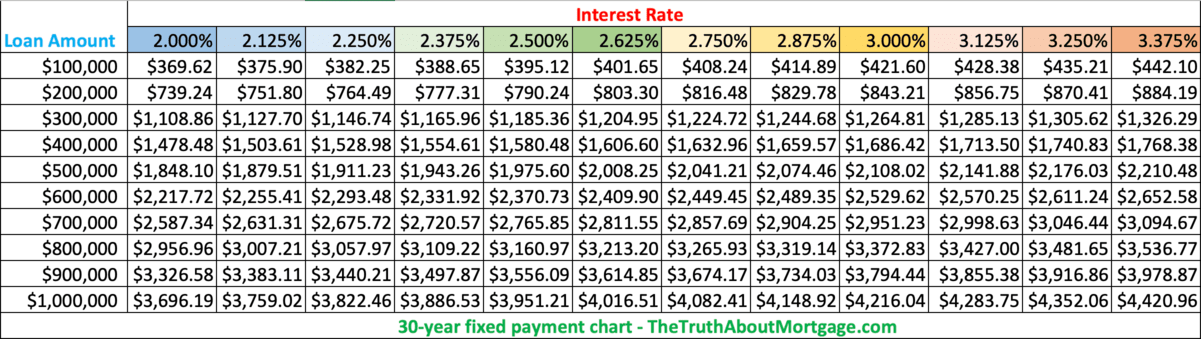

You do not desire this to take place, so do not buy a house up until you have a substantial amount of money to put down. Your home loan rates of interest are figured out by your. Because you're borrowing a lot money, even a small distinction in the rate on your loan will make a huge impact in the total cost of your mortgage in time.

The 7-Minute Rule for Who Took Over Washington Mutual Mortgages

Bad credit can cost you more than $105,000 in interest over the life of the loan, and can raise your regular monthly payment close to $300 monthly. To get the very best rates possible, deal with building credit prior to you use for a home mortgage. You can enhance your credit rating by paying off debt you owe, paying on time, and avoiding opening brand-new accounts or closing old ones.

Likewise, check your credit report to see if there are any mistakes that are harming your rating. Do this well before obtaining a home mortgage since it can take time for mistakes to be repaired. You do not wish to pay countless dollars more on your home mortgage since of a reporting snafu.

Homeownership likewise comes with huge timeshare maintenance fees unexpected costs for house repair work if something fails. That's why having an emergency fund is so crucial prior to getting a home mortgage. Ideally, you must have a fund with 3 to 6 months of living expenses conserved up so you can still pay your bills even if a serious problem takes place.

Little Known Facts About What Was The Impact Of Subprime Mortgages On The Economy.

This may seem like a great deal of money, however you don't want to remain in a house with a roof leakage or handling a job loss and be unable to spend for fixes or make the home mortgage payment. If you don't want to wait to purchase a home up until you've conserved a full emergency situation fund, at least make certain you have a couple of thousand dollars to get you through lean times.

If you have actually got good credit and a strong income, you may be approved to borrow a lot of money. Helpful resources But, just due to the fact that you're approved for a huge loan doesn't imply you need to take it. You probably have great deals of monetary objectives, like retiring some day or paying for college for your kids.